Avalanche vs Snowball (and Other debt Payoff Methods)

Which One Actually Works?

Debt can feel like an insurmountable and suffocating mountain that never gets smaller, and an endless cycle of payments that never seem to make a dent. - especially when you are juggling multiple financial obligations from high interest credit cards, long term student loans, and auto loan payments.

The current average Annual Percentage Rate (APR) for credit cards is about 20%. This high figure is startling for consumers, as it significantly increases the cost of carrying a balance, adding substantially to the principal owed. The 20% average is influenced by Federal Reserve interest rates, issuer risk models, and the variety of credit cards on the market. Cardholders should view this average as a benchmark: a higher APR suggests very expensive debt, while a lower one APR is financially beneficial.

The good news is, there are proven strategies to dig out and build momentum. While the first step is acknowledging the challenge, the important step is tackling the debts head on using battle tested strategy to dig your way out and build powerful financial momentums.

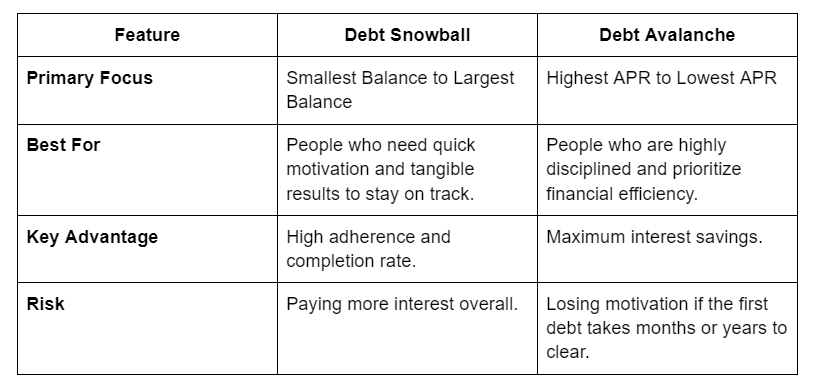

While numerous debt repayment philosophies exist, two methods stand out for their simplicity and effectiveness: the Snowball Method and the Avalanche Method. Both are proven strategies, but they cater to different psychological and financial priorities. The best choice for you hinges on whether you are primarily motivated by rapid psychological wins or maximum long-term cost savings.

❄️ The Snowball Method

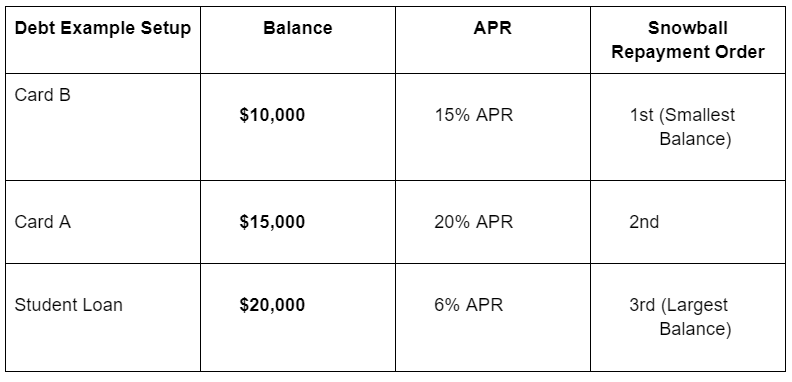

Snowball allows you to pay off debts from the smallest balance to largest, regardless of interest rate. You keep the minimum on all, then throw every extra dollar at the smallest. When its gone, roll that payment into the next smallest and you snowball grows.

The Snowball Method is a psychological approach championed by its focus on building momentum. It instructs you to order your debts based on their balance size, from the smallest to the largest, completely ignoring the interest rate. This strategy prioritizes early, tangible success to keep motivation high.

How the Snowball Method Works:

Pay the Minimums: Commit to paying the minimum required amount on all your debts to avoid fees and maintain good standing.

Order by Balance: List all your debts, ranking them from the smallest total balance to the largest total balance.

Intense Attack: Throw every single extra dollar you can find—from budget surpluses to unexpected windfalls—at the smallest-balance debt. This is your primary focus.

The Roll-Over Effect: Once the smallest debt is completely paid off, you take the entire payment amount (the original minimum payment plus the extra amount you were attacking it with) and roll it into the minimum payment of the next smallest debt. This “snowball” of cash grows with each debt conquered, making payments on larger balances feel significantly easier.

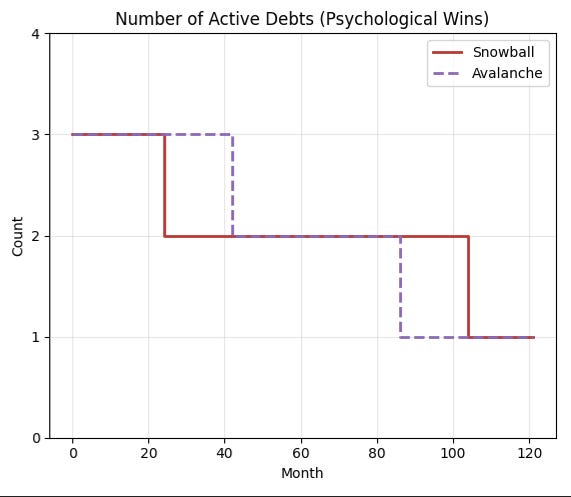

The Psychological Edge: The initial quick wins—wiping out the $10,00 and $15,000 debts relatively fast—provides a powerful, immediate sense of accomplishment that is crucial for maintaining the long, difficult fight against larger debts. High completion rates are often cited as a key benefit because people don’t lose steam.

Pros: Quick psychological wins, strong motivation, higher long-term completion rates, simple to understand and implement.

Cons: May cost more in total interest paid over the life of the repayment plan, as high-interest debts might be paid off later.

⛰️ The Avalanche Method

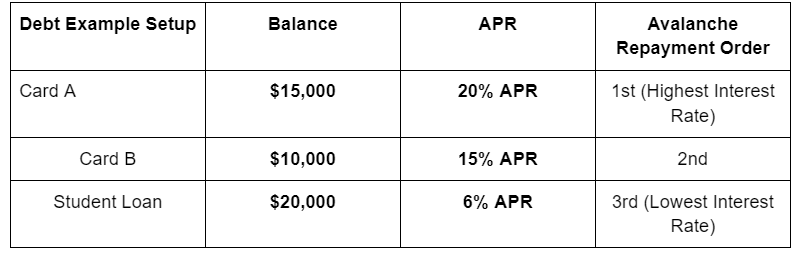

The Avalanche Method is the mathematically superior approach. It focuses strictly on minimizing the total amount of interest you pay over the life of your debt. It instructs you to pay off debts starting with the highest interest rate first, completely regardless of the balance size.

How the Avalanche Method Works:

Pay the Minimums: Just like with Snowball, you must continue to pay the minimum required amount on all debts.

Order by APR: List all your debts, ranking them from the highest Annual Percentage Rate (APR) to the lowest APR.

Intense Attack: Dedicate all of your extra monthly funds to the debt with the absolute highest interest rate. This is the debt costing you the most money every day.

The Roll-Over Effect: Once the highest-APR debt is cleared, you take the entire payment amount you were dedicating to it and roll it into the payment of the debt with the next highest interest rate. This concentration of payments continues until all debts are clear.

The Financial Edge: By aggressively targeting the highest-interest debts first, you immediately reduce the overall interest accrual. Over many years, this method can save hundreds or even thousands of dollars compared to the Snowball Method, potentially leading to a shorter total repayment term.

Pros: Saves the most money on interest, results in the lowest overall cost of debt repayment.

Cons: Might take a long time to see the first debt completely paid off, which can be demotivating if your highest-APR debt also has a large balance. This requires a higher degree of discipline and patience.

The choice between Snowball and Avalanche is fundamentally a trade-off between Psychology (Snowball) and Math (Avalanche).

Ultimately, the most effective debt repayment strategy is the one you will actually stick with until the end. If seeing your debt list shrink rapidly gives you the drive to keep going, the Snowball is your best bet. If the idea of paying a single extra dollar in interest bothers you, the Avalanche is the clear winner. Both methods, executed consistently, are powerful tools for achieving a debt-free life.

⚖️ Other Debt Management Methods

Beyond traditional repayment strategies, several alternative methods can be employed to manage and reduce outstanding debt. These approaches often involve restructuring or refinancing the debt to make it more manageable.

🔄 Debt Consolidation

Debt consolidation is the process of combining multiple high-interest debts, such as credit card balances, personal loans, or medical bills, into a single, new loan. This new loan typically offers a lower interest rate than the average rate of the original debts, a more favorable repayment term, and a single monthly payment.

Mechanism: The new, larger loan is used to pay off all the smaller, existing debts. This simplifies the repayment process, as the borrower now only has one creditor and one due date to manage.

Benefits:

Lower Interest Costs: A primary advantage is securing a lower interest rate, which reduces the total cost of borrowing and speeds up the debt-free date.

Simplified Payments: Managing a single monthly payment instead of several can reduce the risk of missed payments and the associated fees.

Fixed Repayment Schedule: Often, the consolidation loan comes with a fixed term, providing a clear endpoint to the debt.

Common Forms: This can be achieved through a personal consolidation loan, a home equity loan or line of credit (HELOC), or a 401(k) loan (though this carries significant risks).

💳 Balance Transfer

A balance transfer involves moving debt from one or more high-interest accounts (typically credit cards) to a new account, often a new credit card, that offers a lower—frequently 0%—introductory Annual Percentage Rate (APR) for a specific promotional period (e.g., 6 to 21 months).

Mechanism: The credit card issuer pays off the old balances, and the combined amount is then owed on the new card. This effectively pauses the accumulation of interest on the transferred amount during the promotional window.

Benefits:

Interest-Free Repayment: The 0% or low introductory APR allows the borrower to allocate their entire payment toward the principal balance, accelerating the debt payoff.

Short-Term Relief: Provides a window of opportunity to aggressively tackle debt without the compounding effect of high interest.

Considerations:

Transfer Fee: Most balance transfers include a one-time fee, typically 3% to 5% of the transferred amount.

Expiration of Intro Rate: It is crucial to pay off the balance before the promotional period ends, as the APR will revert to a much higher standard rate, which can be detrimental if the debt remains.

🧩 Hybrid Method

The Hybrid Method refers to the strategic combination of multiple debt reduction techniques, tailoring a personalized strategy that leverages the strengths of different approaches to achieve optimal results. This method is highly flexible and dynamic.

Mechanism: A borrower might consolidate their largest high-interest debts (e.g., medical and credit card debt) into a personal loan, while simultaneously using a balance transfer card to pay off a smaller, high-interest credit card balance during a 0% introductory period. They might also apply the “debt snowball” or “debt avalanche” payoff strategies to any remaining smaller debts.

Benefits:

Maximized Savings: By selectively applying the best tool for each type of debt, the borrower can maximize interest savings.

Customized Approach: Allows for a flexible plan that adapts to the borrower’s current financial capabilities, credit profile, and specific debt structure.

Sustained Momentum: The variety of methods can help maintain motivation by showing progress on different fronts simultaneously.

📊 What the numbers say

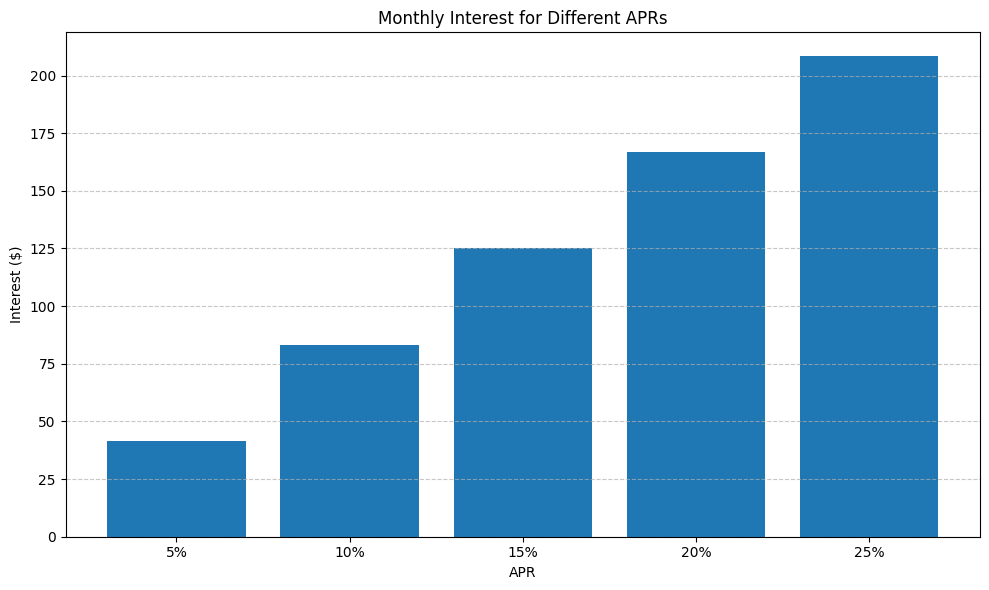

The Annual Percentage Rate (APR) represents the yearly cost of the loan, expressed as a rate. A crucial point of understanding is that while the APR is a yearly rate, its impact is calculated on a daily basis.

Here is a detailed breakdown of the calculation process:

Determining the Daily Periodic Rate (DPR): The APR is not applied directly to the balance monthly. Instead, it is first divided by 365 (the number of days in a year) to determine the Daily Periodic Rate (DPR).

DPR = APR / 365Daily Interest Calculation (Compounding): This DPR is then applied to the average daily balance of the loan or credit account. The calculation is performed every single day, leading to a process known as daily compounding. This means that the interest accrued on one day becomes part of the balance on which interest is calculated for the next day, though it’s not applied until the statement.

The Average Daily Balance Method: Lenders typically use the average daily balance to ensure fairness. This is calculated by taking the sum of the outstanding principal balance for each day in the billing cycle and dividing that total by the number of days in the billing cycle. The daily interest charge is calculated as:

Daily Interest=Average Daily Balance × DPRAccrual vs. Application: While the interest accrues (is generated and tracked) daily through this compounding process, it is not actually added to the principal balance on a daily basis. The cumulative total of the daily interest charges for the entire billing cycle is calculated and then officially applied (posted) to the account’s balance only once, at the end of the billing cycle, when the monthly statement is delivered. This is the amount that appears as the “Interest Charge” on the statement.

In summary, the APR governs the rate, the DPR facilitates the daily compounding, and the average daily balance determines the principal amount the rate is applied to, ultimately dictating the total interest that “adds up” and is finally charged to the borrower’s account each month.

The provided example clearly demonstrates the impact of varying Annual Percentage Rates (APRs) on a fixed $10,000 principal balance, illustrating how the daily interest charge and monthly accrual increase linearly with the APR. Specifically, as the APR rises from 5% to 25%, the daily interest charge climbs from $1.37 to $6.85, highlighting that a debt at 20% APR costs four times as much in daily interest as one at 5% APR. This numerical relationship underscores the foundational principle behind effective debt reduction strategies like the Avalanche Method, proving that targeting and eliminating the highest-APR debt provides the most significant immediate savings due to the reduction in the daily compound interest burden.

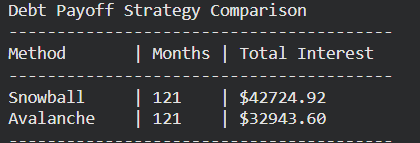

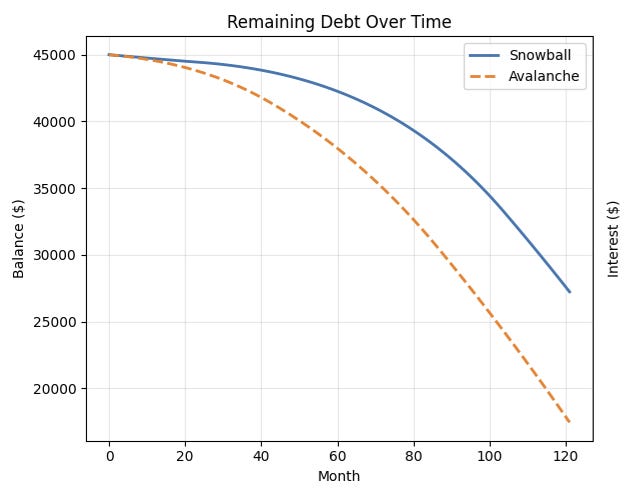

When analyzing the repayment strategies for the outstanding debt, a clear comparison emerges between the Snowball and Avalanche methods. Based on the previous examples of our current total debt burden, both methods predict a nearly identical timeline for complete debt elimination. Specifically, it is projected that achieving a debt-free status will take approximately 121 months, which translates to just over ten years.

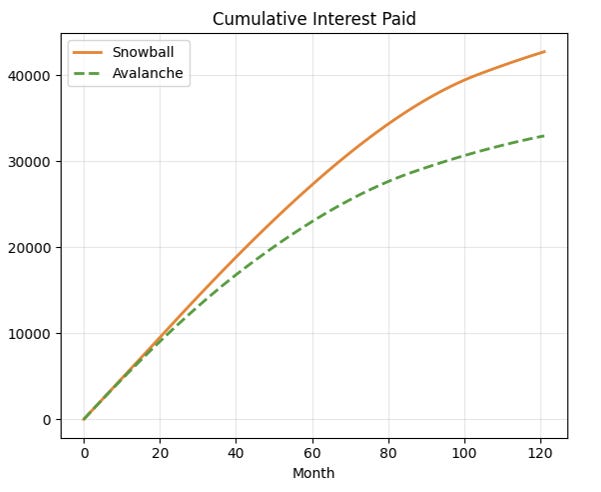

The analysis shows a substantial disparity in the total interest paid: a difference of $9,781.32 separates the two approaches.

While the time frame for repayment is consistent across both strategies, the significant difference lies in the total amount of interest paid over that period. The core distinction between the Snowball method (which prioritizes paying off the smallest debts first) and the Avalanche method (which targets debts with the highest interest rates first) directly impacts the financial cost of the debt.

The Avalanche method is the mathematically optimal strategy for debt reduction because it minimizes the total interest paid. This approach targets the debt with the highest interest rate first, regardless of the principal balance. By focusing maximum resources on the most expensive debt, it achieves a faster reduction in remaining debt.

Once the highest-interest debt is paid off, the funds are immediately applied to the minimum payment of the next-highest interest debt. This accelerates the payoff process and significantly reduces the cumulative interest paid over time.

While the repayment period remains consistent (121 months in this analysis), the Debt Avalanche method is financially superior to the Snowball method, which would result in higher total interest costs. This confirms the efficiency of the committed repayment structure itself, but highlights the financial advantage of the Avalanche method over methods often preferred for psychological reasons.

The core advantage of the “snowball method” for debt repayment lies in its psychological and mathematical mechanics, leading to a notably faster and more satisfying path to becoming debt-free. This accelerated success is primarily driven by the initial strategy of targeting smaller debts first. By focusing all extra principal payments on the smallest balance, a borrower achieves a quick “win” or early success, eliminating an entire debt relatively rapidly. This initial victory provides a significant psychological boost, building momentum and confidence in the repayment plan.

Once the smallest debt is paid off, the amount of money previously allocated to that debt’s minimum payment is not reallocated elsewhere; instead, it is “rolled over” and added to the minimum payment of the next smallest debt. This process creates an ever-increasing payment amount dedicated to the principal of subsequent debts, much like a snowball rolling down a hill and growing in size and speed.

This systematic application of the freed-up funds ensures that each subsequent debt is tackled with a larger combined payment, dramatically accelerating its payoff timeline. The compounding effect of rolling over the cleared minimum payments is what mathematically solidifies the snowball method’s ability to show a faster win, turning initial psychological momentum into a sustainable, high-velocity debt-reduction mechanism.

🧠 Bottom line

The key to successfully tackling debt lies not just in the mathematical efficiency of a method, but fundamentally in the sustainability of the system you adopt. The “best” method is, unequivocally, the one you are committed to following consistently and persistently until victory is achieved.

Your psychological profile and financial goals will dictate the superior choice:

If you are motivated by quick, visible achievements and need constant psychological reinforcement to maintain momentum, the Snowball Method is likely your champion. This strategy focuses on paying off the smallest debts first, regardless of their interest rate. The immediate “quick wins” of eliminating entire debts provide a powerful psychological boost, generating the motivation needed to stay the course, rolling the payment from the eliminated debt onto the next smallest one, like a snowball gaining mass.

Conversely, if you possess a high degree of discipline, are laser-focused on optimizing your finances, and prioritize mathematical efficiency, the Avalanche Method will minimize the total interest paid. This strategy involves ranking debts by their interest rate and aggressively paying down the one with the highest rate first. While the initial progress may feel slower because the highest-interest debt is often larger, the long-term financial benefit is substantial, as you systematically halt the most costly drain on your wealth.

Regardless of the method chosen, you are actively building a robust financial system. This systematic approach is the core mechanic of wealth building. It fundamentally changes your relationship with money, initiating a powerful, transformative shift that moves your financial status from a position of surviving (debt maintenance, living paycheck-to-paycheck) to one of growing (debt elimination, asset accumulation, and true financial independence). The system itself—the habit of dedicating surplus cash flow to a deliberate financial goal—is the lasting mechanism that secures your future.